A few of our purchasers undergo an IPO and are available out the opposite finish financially unbiased. Thirty-five years outdated, with $10M within the financial institution? Examine. (Technically, not the financial institution, however a broadly diversified, low-cost portfolio. At the least, that’s the hope!)

Others of our purchasers undergo an IPO and are available out the opposite finish with a pleasant chunk of change, but it surely’s not “by no means should work once more” cash.

And but others of our purchasers by no means undergo an IPO, however steadily squirrel away a lot of {dollars}, yr after yr, from their high-paying tech jobs. For instance, when you’ve labored for Apple for the final 10 years, you don’t want an IPO to have had the power to construct fairly the nest egg simply from saving a goodly portion of that RSU revenue.

Everybody kinda needs to be in that first class of “in a single day monetary independence.” However that’s virtually at all times outdoors of our management. I’ve began speaking with increasingly of our purchasers in regards to the next-best factor to full monetary independence: “Coast FIRE” (Monetary Independence Retire Early). (I cringe in any respect the FIRE jibber jabber within the personal-finance house, however that is merely probably the most succinct strategy to focus on the phenomenon, so forgive me!)

Coast FIRE is the state of funds the place you don’t must add to your retirement financial savings anymore, so long as you don’t withdraw from it. Which means that, sure, it’s important to have a job that pays to your present life-style (and taxes, in fact)…however that’s it. Which actually opens up the world of job prospects!

This depends closely on the ability of compounding.

The Energy of Compounding

You ever hear the bit about how 99% of Warren Buffet’s (astronomical) wealth got here after the age of fifty? That’s attributed largely to easily Letting It Develop.

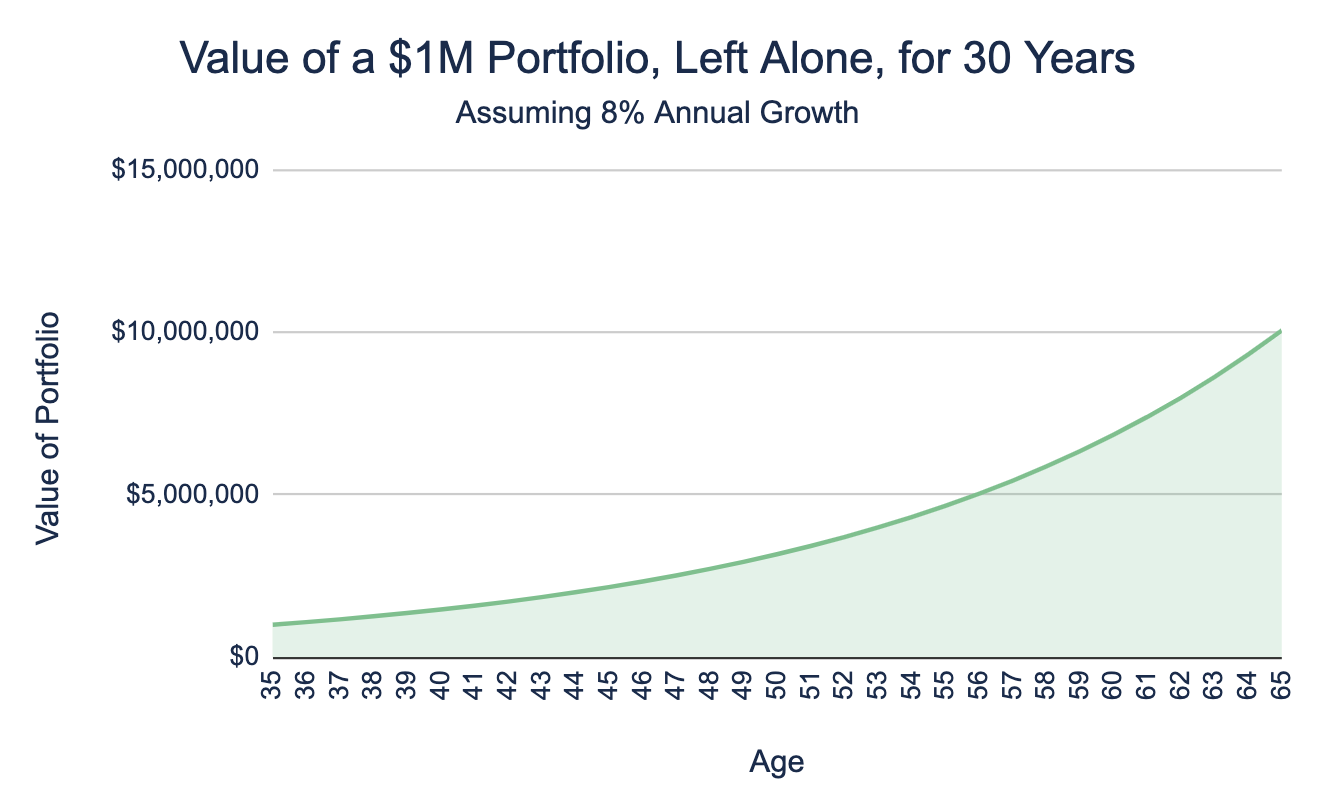

Let’s say your portfolio is price $1M now. In case you are in your 30s and 40s, you may’t stop working and reside on that for the following 5 to 6 a long time of retirement. (I imply, I suppose somebody can, however the life-style sacrifices are ones that few individuals I do know are keen to make.)

Nevertheless, try what occurs if we make investments that $1M and let it develop from the age of, say, 35 to 65 (30 years):

From the age of 35 to 56 (21 years), it grows from $1M to roughly $5M. After which in simply the following 9 years (age 56 to 65), it grows from $5M to only over $10M.

Fairly good if you haven’t put a single further greenback into it, eh?

That is the place placing your cash in a low-cost, diversified portfolio, largely in shares, after which Not Getting Fancy is available in.

Understand that our human brains don’t intuitively settle for compounding. You actually have to have a look at numbers and charts and hope your rational mind can override your lizard mind.

The Evaluation We Do With Our Purchasers

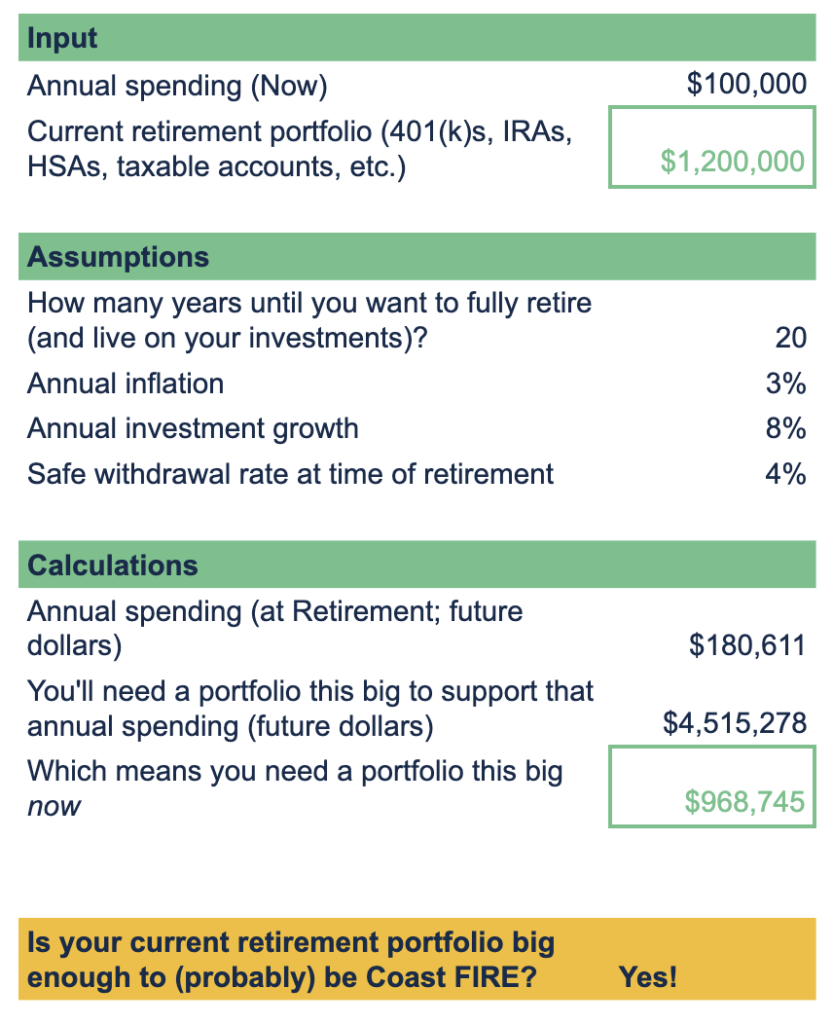

That is how we determine whether or not our purchasers are in that enviable “I can cease saving” place:

We determine how a lot you at present spend and the dimensions of your retirement funding portfolio. Your retirement portfolio may include solely your present 401(ok), or it is perhaps an advanced mess (a slew of 401(ok)s, a standard IRA, a Roth IRA, an HSA, and a taxable funding account…all of that x 2 when you’re a pair). No matter.

We make some assumptions (aka, greatest guesses) about some important items of data. To clarify slightly additional about every of those numbers:

- How lengthy from now do you need to totally retire and begin dwelling in your investments?

- Inflation has traditionally been a mean of three% per yr.

- An 8% annual progress price is an inexpensive guess based mostly on historic numbers, and naturally it relies on what precisely you’re invested in.

- What’s going to your protected withdrawal price be in retirement? That’s, what proportion of your portfolio are you able to safely withdraw annually and nonetheless be assured you received’t run out of cash by the point you die?

Historically, this has been 4%, based mostly on the unique, seminal analysis within the early Nineties, by William Bengen. There have been a ton of follow-on research and analysis that tweak this quantity based mostly on how lengthy your retirement shall be or with how a lot you’re keen to cut back your withdrawals in years when your portfolio does poorly.

We calculate the dimensions of the portfolio you want now to get to monetary independence then (i.e.,at your retirement age), years down the highway. This depends on current worth and future worth calculations, that are too laborious by hand however a cinch by spreadsheet system or monetary calculator.

Is your precise present retirement portfolio greater than what we simply calculated you want?

In that case, congratulations! You may have probability of not needing to save lots of any extra money for retirement.

If not, welp…that you must save extra. Or plan to work longer. Or decrease your bills. (There are solely so many levers to achieve monetary independence, and these are the essential three.) You’ll be able to in all probability use one of many umpteen on-line Coast FIRE calculators to see how shut you’re, how for much longer, and what number of extra {dollars} that you must save to get there.

Word: There are a ton of Coast FIRE calculators on the web. They usually’re in all probability simply tremendous (with a method higher UI and UX than our spreadsheet). I imply, the logic and math aren’t that difficult (from a finance-nerd PoV). However as a result of I don’t see how they’re programmed, I can’t reliably suggest them. The evaluation we do with our purchasers might be precisely the identical; it simply occurs to be underneath our management.

You Can Cease Saving. Now What?

THIS IS THE WHOLE POINT.

What new alternatives or desires or pleasure can this open up for you?

In the event you solely must earn sufficient cash to pay your taxes and your payments, and no extra saving, possibly meaning you may earn $20k, $40k, $60k, $100k much less per yr.

What sort of job would you be keen to pursue in case your compensation wants had been that a lot decrease?

Now you can begin fascinated with your profession, your work life, although a way more beneficiant lens! That job that sounds significant to you? Or takes up much less of your time, so you may work out extra or volunteer or spend time with household? Nevertheless it doesn’t pay as a lot? So long as it pays sufficient to easily cowl your bills, you may take it!

Make Positive You Don’t Increase Your Spending

In the event you’ve been making $300k/yr, and also you’ve reached Coast FIRE, nice! You don’t have to save lots of any extra. Your present investments, if left to compound over a few years, ought to be sufficient to cowl your spending on the time you begin dwelling off of your investments.

To date, so good.

However let’s say you’re accustomed to beginning with $300k, paying some taxes, saving a few of it, after which spending the remainder. Once we take away the saving from that equation, what’s left over to spend is method method greater.

In the event you get accustomed to spending that method greater quantity, now you really need far more cash sooner or later to cowl this now-much-more-expensive life-style.

So listen. Possibly you discover that you could spend some extra, however you’ll nonetheless proceed saving, simply much less. And the continued saving (although lower than earlier than) ought to be sufficient to make up for the upper (although not all that a lot increased) spending.

Or possibly you permit that $300k/yr job and take an $80k/yr job at your favourite non-profit (as a shopper just lately instructed me she had thought of). Now even when you don’t save something, the cash you have got accessible to spend is method method much less, and this danger is moot (so long as you’re not touching your retirement portfolio).

Preserve Room for Error, and Make Changes Alongside the Approach

I don’t encourage you to chop this evaluation shut. On the age of 35 or 45…or 65, there are nonetheless method too a few years forward of you throughout which too many unpredictable issues might occur that will render your calculations out of date.

The declaration of your “Coast FIRE” standing is based on you making fairly correct assumptions about:

- how lengthy you’ll go away the portfolio to develop earlier than you retire. Even when you one way or the other knew if you wished to retire (which, in my view, is unlikely various years out), lots of people find yourself retiring sooner than they’d deliberate, typically resulting from well being or incapacity. (The 2021 Retirement Confidence Survey (the thirty first annual), by the Worker Profit Analysis Institute (EBRI) and Greenwald Analysis, recorded that 47% of individuals fall into this class.)

- how a lot your portfolio grows annually

- how a lot you spend annually (which in flip relies upon, partly, on inflation)

Sadly, one factor I can virtually assure you is that there isn’t any method that you could reliably predict these numbers two to 3 a long time out. So, be a bit conservative in your assumptions.

In the event you’re at Coast FIRE with a 9% funding progress price, what occurs if there’s solely 7% progress? What occurs if inflation is 4% as an alternative of three%? What occurs when you’re pressured to retire in 15 years as an alternative of 20?

No matter your present Coast FIRE standing, even when it has loads of room for error, Life Nonetheless Occurs. For the great or the unwell. This is the reason you don’t run this evaluation as soon as if you’re 35 or 40 after which ignore it for the following 20 years. You need to examine in each one or few years (relying on simply how a lot life is occurring).

Possibly you discover that you must begin saving once more. Or in the reduction of in your bills. Possibly you discover you’re even extra solidly Coast FIRE and due to this fact can plan to completely retire earlier. Or begin dwelling now on a small quantity of withdrawals out of your funding portfolio so as to add to the revenue out of your job.

I feel it’s healthiest to have an perspective of “I’m in all probability Coast FIRE” versus “I’m positively Coast FIRE.” After which take a look at that speculation usually.

Implications for When You’re Youthful/Earlier in Your Profession

Monetary recommendation has lengthy been of the kind “Save as a lot as you may as younger as you may. Pinch your pennies! Delay your gratification!”

It’s not precisely thrilling or motivating recommendation for individuals earlier of their careers.

Then we’ve got a brand new era of monetary people, from licensed monetary advisors to influencers like Ramit Sethi, who’re all, “Whoa whoa whoa WAIT a minute. There’s a strategy to get pleasure from your life now and nonetheless be accountable about your future. In any case, you by no means understand how lengthy you have got on this planet, and it’d be a disgrace to by no means get to that future you’re scrimping and saving for!”

I very a lot recognize this extra humane—and doubtless finally efficient—strategy to non-public funds.

That stated, let me summon some good quaint “Ack, save early and sometimes!” power.

What we will see on this submit is that the sooner you begin investing cash, and the extra money you make investments early, the earlier you may cease worrying about it. The earlier your job can cease specializing in “how a lot does it pay?” and begin specializing in “what sort of life and that means does it afford me?”

Now, there’s at all times a steadiness, proper? You’ll need to match this choice to who you already are. In case you are frugal by nature, and end up pinching pennies in an effort to save and make investments extra, properly, you’ll in all probability profit from loosening the purse strings a bit and having fun with life extra now. In the event you haven’t given a thought to saving for the longer term or solely put sufficient into your 401(ok) to get the match, properly, then, you in all probability need to kick it up a notch, because the Clever Emeril as soon as stated.

Coast FIRE is just one path—of many—to extra freedom in your life and selection in your profession. But when you end up there, whoo! Now, I ask you:

How are you going to use this freedom to alter your life in order that it’s extra aligned together with your values?

In the event you assume Coast FIRE is perhaps a path that matches your scenario and also you need to discover additional, please attain out and schedule a free session or ship us an e-mail.

Join Circulate’s twice-monthly weblog e-mail to remain on high of our weblog posts and movies.

Disclaimer: This text is supplied for academic, basic info, and illustration functions solely. Nothing contained within the materials constitutes tax recommendation, a advice for buy or sale of any safety, or funding advisory companies. We encourage you to seek the advice of a monetary planner, accountant, and/or authorized counsel for recommendation particular to your scenario. Copy of this materials is prohibited with out written permission from Circulate Monetary Planning, LLC, and all rights are reserved. Learn the complete Disclaimer.

{kind=link}