In the present day’s put up was cowritten by Peter Essele, vice chairman of funding administration and analysis.

Within the massive image, the inflation we’re now seeing could possibly be a brief phenomenon, pushed by a a lot quicker restoration from the pandemic than anticipated, mixed with the standard snafus because the world financial system tries to spin up rapidly. Certainly, these results are actual.

However earlier than we discover that concept additional, my colleague Pete Essele recommended we first ask a greater query: is that scary inflation print actually as unhealthy because it seems to be? In different phrases, earlier than we begin on the lookout for causes for the issue, maybe we wish to first make certain the issue is actual. And whenever you break down the numbers? The inflation risk doesn’t look so unhealthy in spite of everything.

Pete’s Take

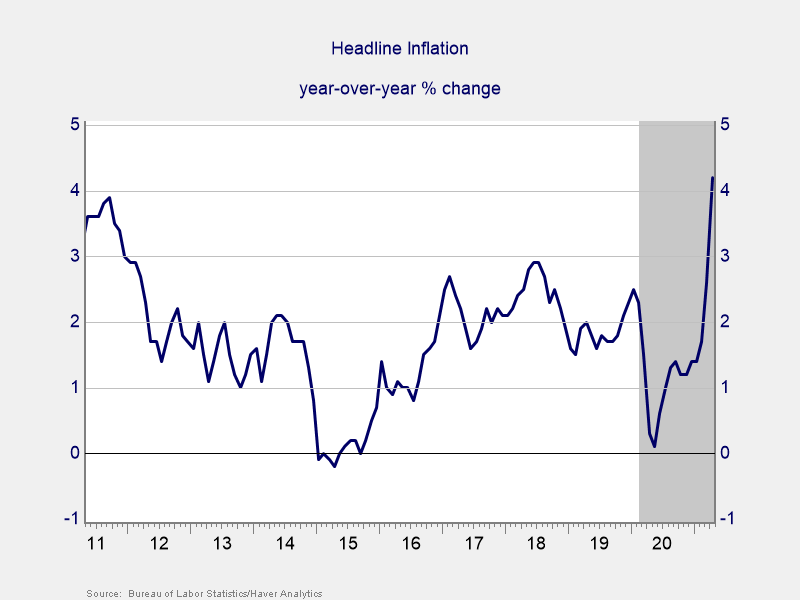

Final week’s inflation print (Client Worth Index or CPI) got here in at 4.2 % year-over-year, the biggest enhance since 2008. Buyers are actually questioning if maybe it is sensible to start shopping for inflation-sensitive property like TIPS (U.S. Treasury inflation-protected securities), commodities, and treasured metals. Earlier than doing so, it’s vital to grasp the numbers as a result of, like many financial information factors, the satan’s within the particulars. Let’s take a look.

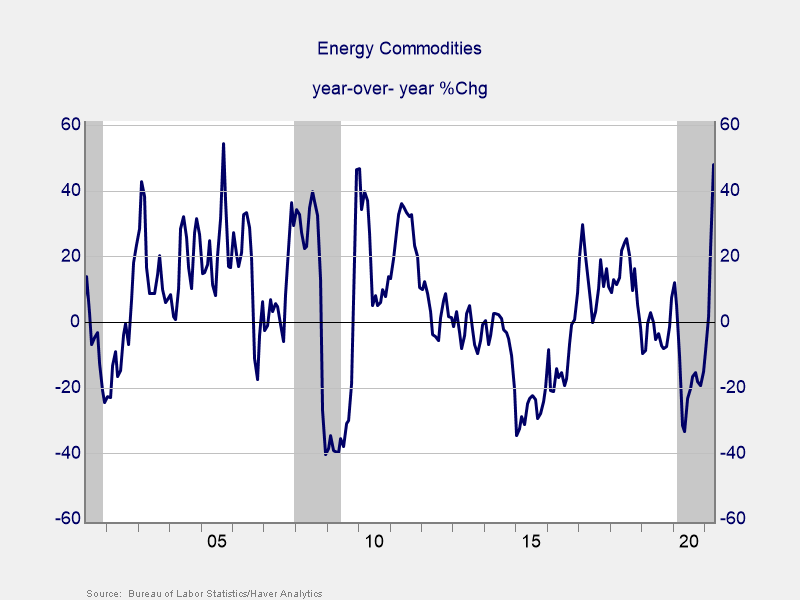

Headline inflation. Though the 4.2 % rise in costs over the previous yr was a noteworthy print, the numbers counsel that it wasn’t a broad-based enhance throughout all items and companies. In truth, of the main expenditure classes used to calculate the headline quantity, only some got here in above 4.2 %. Power commodities, used automobiles and vehicles, and transportation companies (particularly, airfare and car insurance coverage) stood out, which noticed yearly value will increase of 47.9 %, 21 %, and 5.6 %, respectively. All different main expenditures had been according to long-term averages. The three aforementioned classes account for under 12 % of the CPI basket of products and companies. As a result of they skilled such vital will increase, the general headline quantity was pulled greater, touchdown above latest averages. The biggest part of CPI (shelter) got here in at 2.1 %, in contrast with a 10-year common of two.76 %.

Power commodities. What additionally must be thought-about within the numbers, particularly for vitality commodities, is that present costs are being in contrast with a very low base, which makes year-over-year values look vital. As an illustration, the worth of oil at present stands at pre-COVID ranges ($62 per barrel) after plunging to low double digits in April 2020 because the financial system got here grinding to a halt. With enhancements within the financial setting as of late, costs have began to normalize from historic lows. Subsequently, a prudent investor ought to assess present value ranges in contrast with long-term averages and never take the year-over-year will increase at face worth.

Brad Breaks It Down

Thanks, Pete. For many who acquired misplaced within the numbers, most gadgets within the CPI got here in below, in lots of instances nicely below, the 4.2 % headline quantity. That scary print was largely as a result of a handful of classes that spiked, notably vitality, after collapsing final yr. In different phrases, that scary quantity was a one-off.

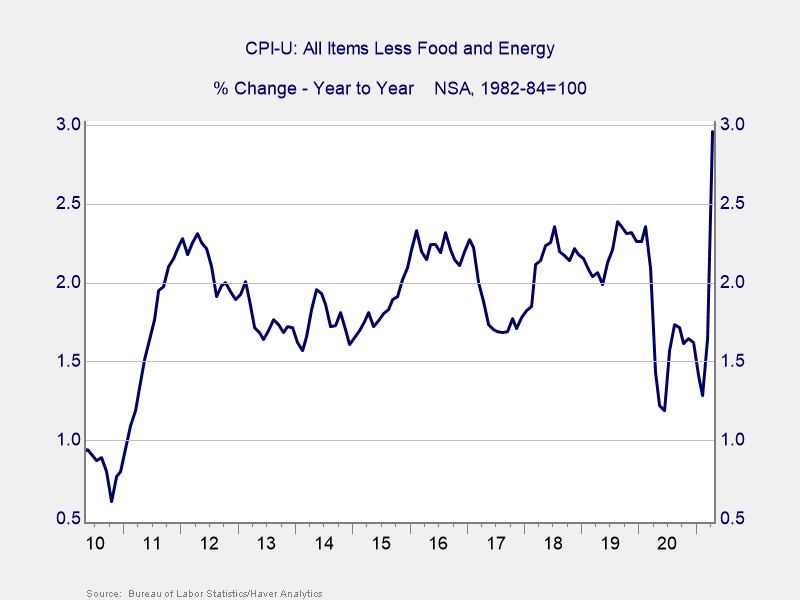

Core inflation. A less complicated approach to take a look at it’s to take out meals and vitality from the headline quantity, which will get us to what’s known as core inflation. If we have a look at that, the 4.2 % turns into 2.96 %, which remains to be not nice however is significantly much less scary than the preliminary headline quantity. Power alone accounts for an excessive amount of the rise, and that’s as a result of collapse and rebound in costs over the previous yr.

General change in value. All nicely and good, I hear you say, however I have to warmth my residence and gasoline my automotive. I can’t take out vitality! Honest sufficient. So let’s take out the vitality value plunge final yr and the restoration this yr by going again and seeing what the general change in costs has been over the previous two years. And what we see, within the chart under, is that costs are up about 4 % total since two years in the past, which is about the identical as we noticed in 2018 and 2019. For those who take out the pandemic results, inflation seems to be very similar to it did in 2019. This isn’t a surge in inflation; slightly, it’s a return to regular. Pete was fairly proper to ask the query as a result of once we dig into the small print, inflation shouldn’t be almost as scary because the headline quantity would counsel.

Inflation Not That Scorching

Now there are indicators that inflation might rise within the coming years. The infrastructure issues are actual and can want time to right. Labor shortages may turn out to be extra frequent, which might drive up inflation. And as globalization slows or reverses, inflation will even possible rise. These are actual issues to look at for over the subsequent couple of years.

However that isn’t what is going on now. Whenever you dig into the numbers, inflation merely isn’t that sizzling. Whenever you look over an extended interval than the trough to peak of the previous yr, once more, inflation merely isn’t that sizzling. And when you think about the actual issues the worldwide financial system is coping with, the shock is that inflation shouldn’t be greater.

As soon as once more, stay calm and keep it up.

Editor’s Be aware: The unique model of this text appeared on the Unbiased Market Observer.

{kind=link}