")

It’s a superb apply to take an intensive evaluation yearly of funding efficiency together with charges and taxes. A dual-income family might accumulate a half dozen or extra accounts due to tax traits, possession, and targets. A great way to begin is to checklist the accounts so as of deliberate withdrawals. The following step is to be sure that every account has the suitable quantity of threat and that the belongings inside are tax-efficient for the kind of account. I’m within the strategy of changing Conventional IRAs to Roth IRAs and the conversion is taxed as peculiar revenue. Municipal Bonds are included in Modified Adjusted Gross Revenue and will impression Medicare Premiums (IRMAA). In after-tax accounts, revenue is taxed whereas inventory appreciation shouldn’t be till offered after which usually at decrease capital positive aspects charges. This is called the Bucket Strategy.

Our evaluation discovered that we have been paying over one p.c of belongings to have one particular objective, after-tax account managed with a 50% Inventory to 50% Municipal Bond Ratio. It’s a comparatively small, however vital account that I had arrange throughout unsure occasions to be tax environment friendly. Within the hierarchy of withdrawals, it will likely be the final account tapped. The suitable objective for this account is for capital appreciation and ease whereas minimizing taxes. I exploit Constancy and Vanguard wealth administration providers for a few of our investments, and within the context of general portfolio administration, I’m on the lookout for a single tax-efficient fairness fund to “purchase and maintain” for this account.

This text is split into the next sections:

Funding Goal

Collectively, my investments resemble a 60% inventory/40% bond diversified portfolio, partly as a result of I’ve pensions and Social Safety to cowl most residing bills and might stand up to down markets. I focus Bucket #1 (Residing Bills) on short-term money equivalents corresponding to municipal cash markets and bonds. Bucket #2 is generally Conventional IRAs the place taxes are but to be paid and which have greater allocations to taxable bonds. Lengthy-Time period Bucket #3 consists of Roth IRAs and After-Tax Accounts that are concentrated in equities which might be tax-efficient if held for the long run or utilizing tax loss harvesting.

My targets for this one fund are 1) to have excessive after-tax returns, 2) to reduce revenue and taxes, and three) to have respectable risk-adjusted returns as measured by the MFO Score. This sometimes means an fairness fund that pays low dividends and has low turnover.

Search Standards

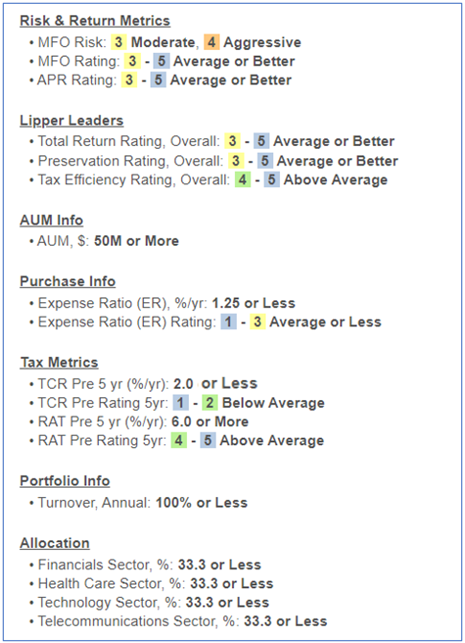

Desk #1 exhibits the factors that I used for the preliminary search. I restricted the mutual funds to Constancy and Vanguard. Whereas volatility shouldn’t be a serious consideration for this fund, I needed to get rid of essentially the most risky funds.

Desk #1: Search Standards For Tax-Environment friendly Funds

Supply: Creator utilizing MFO Premium Fund Multiscreener & Lipper International Knowledge Feed

Abstract Of Lipper Classes

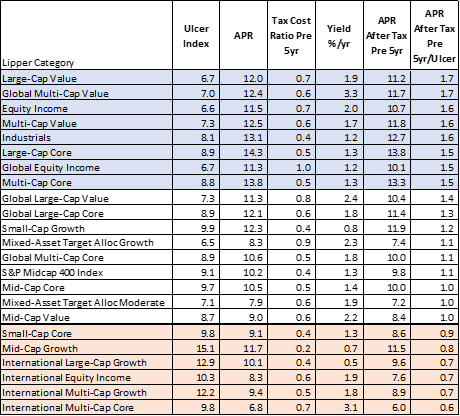

After a strategy of elimination, the search resulted in 32 mutual funds, and eighty-four exchange-traded funds in twenty-three Lipper Classes as proven in Desk #2. The classes are sorted from the very best five-year After-Tax Annualized Return/Ulcer Index. The Ulcer Index is a measure of the depth and period of drawdowns. The highest part shaded in blue accommodates the Lipper Classes that I’m most desirous about, however I additionally wish to contemplate international funds from the center part.

Desk #2: Tax-efficient Lipper Classes

Supply: Creator utilizing MFO Premium Fund Multiscreener & Lipper International Knowledge Feed

Quick Listing of Tax-Environment friendly Funds – 5-Yr View

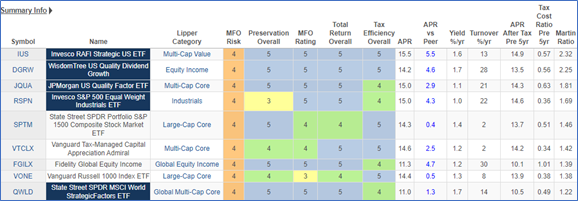

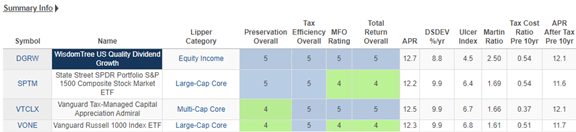

I then went via the funds in every of the Lipper Classes and chosen one or two primarily based on after-tax return, fund household score, and tax effectivity, amongst different standards. The 9 funds in Desk #3 are excellent tax-efficient funds.

Desk #3: Quick Listing of Tax-efficient Funds – 5 Years

Supply: Creator utilizing MFO Premium Fund Multiscreener & Lipper International Knowledge Feed

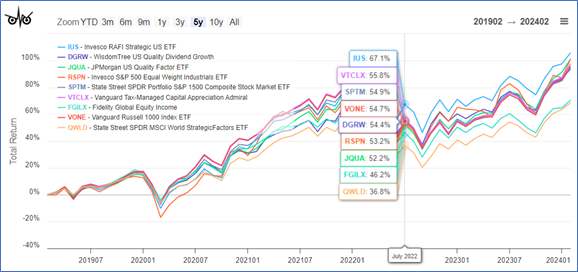

Determine #1 exhibits the five-year efficiency of those funds. The 2 international funds have underperformed, however this doesn’t concern me due to stretched valuations within the US.

Determine #1: Efficiency of Quick Listing of Tax-efficient Funds – 5 Years

Supply: Creator utilizing MFO Premium Fund Multiscreener & Lipper International Knowledge Feed

Closing Listing of Tax-Environment friendly Funds – Ten-Yr View

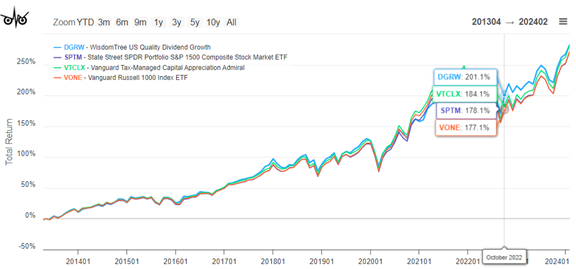

I then appeared on the funds over a ten-year interval. All the funds in Desk #4 are excellent, however I favor Vanguard Tax-Managed Capital Appreciation (VTCLX) and WisdomTree US High quality Dividend Progress (DGRW). Determine #2 exhibits the ten-year efficiency of those funds.

Desk #4: Closing Listing of Tax-efficient Funds – Ten Years

Supply: Creator utilizing MFO Premium Fund Multiscreener & Lipper International Knowledge Feed

Determine #2: Efficiency of Closing Listing of Tax-efficient Funds – Ten Years

Supply: Creator utilizing MFO Premium Fund Multiscreener & Lipper International Knowledge Feed

Vanguard Tax-Managed Capital Appreciation (VTCLX)

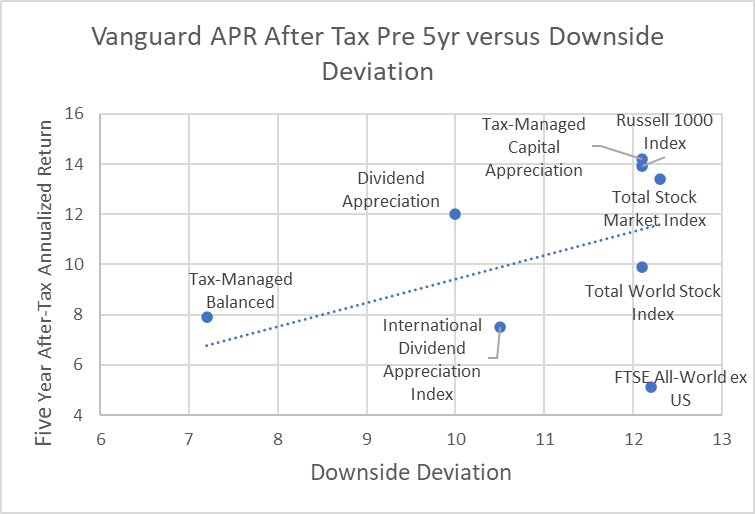

I made a decision to put money into the Vanguard Tax-Managed Capital Appreciation Admiral Fund (VTCLX). The hyperlink to the documentation is right here. Determine #3 exhibits how VTCLX compares to different Vanguard funds for After-Tax Returns versus Draw back Deviation. It has excessive after-tax returns however roughly matches the whole marketplace for volatility.

Determine #3: APR After-Tax Pre-5Year Versus Draw back Deviation

Supply: Creator utilizing MFO Premium Fund Multiscreener & Lipper International Knowledge Feed

Product Abstract

“As a part of Vanguard’s sequence of tax-managed investments, this fund affords buyers publicity to the mid- and large-capitalization segments of the U.S. inventory market. Its distinctive index-oriented strategy makes an attempt to trace the benchmark whereas minimizing taxable positive aspects and dividend revenue by buying index securities that pay decrease dividends. One of many fund’s dangers is its publicity to the mid-cap section of the inventory market, which tends to be extra risky than the large-cap market. Buyers in a better tax bracket who’ve an funding time horizon of 5 years or longer and a excessive tolerance for threat might want to contemplate this fund complementary to a well-balanced portfolio.”

Fund Administration

Vanguard Tax-Managed Capital Appreciation Fund seeks a tax-efficient whole return consisting of long-term capital appreciation and nominal present revenue. The fund tracks the efficiency of the Russell 1000 Index—an unmanaged benchmark representing large- and mid-capitalization U.S. shares. The advisor makes use of portfolio optimization strategies to pick a pattern of shares that, within the mixture, mirror the traits of the benchmark index. The method emphasizes shares with low dividend yields to reduce taxable dividend distributions. As well as, a disciplined promote course of minimizes the belief of internet capital positive aspects and will embody the belief of losses to offset unavoidable positive aspects. The expertise and stability of Vanguard’s Fairness Index Group have permitted steady refinement of indexing strategies designed to reduce monitoring error and supply tax-efficient returns.

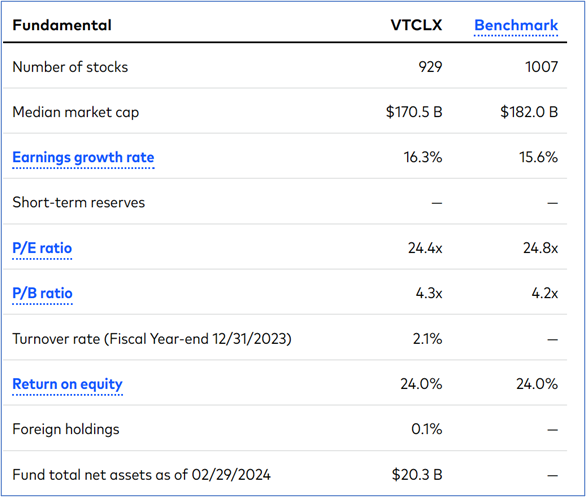

Desk #5 accommodates the basics for VTCLX and Desk #6 accommodates the sector allocations.

Desk #5: VTCLX Fundamentals

Supply: Vanguard

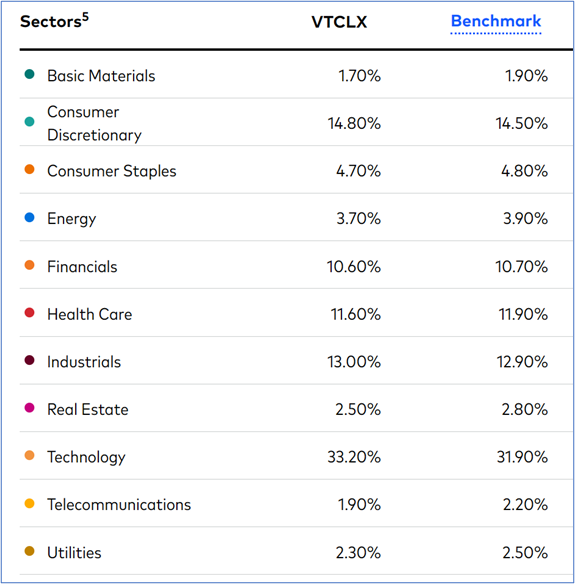

Desk #6: VTCLX Sector Allocation

Supply: Vanguard

Closing

Over the subsequent ten years, changing this 50% Inventory/50% Bond account to DIY with one fairness fund ought to lead to saving 1000’s of {dollars} in charges, improve returns, and cut back taxes. It suits into an general balanced portfolio and meets my aims of holding it easy. At the moment, this account has a mix of high quality ETFs. I’ll steadily convert them over to the Vanguard Tax-Managed Capital Appreciation (VTCLX) when market situations are favorable.

{kind=link}