Introduction:

Within the March 2024 MFO, I launched the 2 principal developments in Choices in recent times.

Zero-Day Choices and Choices-Primarily based Funds. We learnt concerning the historical past of choices, the market gamers concerned and benefitting from Choices, and began getting deeper into the Funds.

In April MFO, via the twond and threerd articles within the collection, I hope to dive deeper into Choices-based funds.

On this article, I wish to perceive the motivations of the traders in these funds and of the fund managers concerned. We wish to have a look at a small collection of these funds qualitatively so we will admire the variety inside the Choices Primarily based Fund universe.

From Shares & Choices to Choices-based Funds

Choices consumers have one among two objectives in thoughts: leverage or safety.

Possibility sellers are on the opposite facet of this coin. By underwriting safety or leverage, choice sellers are rewarded with choice premium, which is repackaged and known as “revenue” by some.

Choices-based funds have two parts:

- The primary is to choose an fairness sleeve: S&P 500 Index, Giant Caps, Worth shares, Nasdaq, Actively Managed or Passive, and so forth.

- The second is to repackage the three themes of choices market gamers: leverage, safety, and revenue.

Each Choices fund is a mix of an Fairness Sleeve and an Choices technique.

A Twist in Time

Equities are thought of everlasting devices. If an organization survives in its present kind, the inventory lives on completely. As soon as an investor buys a inventory, there may be nothing additional to do to protect the standing as a partial proprietor of the enterprise and earn its income and dividends.

Not so with Choices. Every Possibility comes with a time-frame. Zero-day choices actually expire the identical day (0 days). A 1-year choice expires after a yr, and so forth.

A Twist in Strike/Worth

An investor is an extended inventory at no matter worth they purchase the inventory.

Not so with Choices. Every Possibility comes with a Strike Worth. On the Possibility expiry, one compares the Strike worth of the Possibility vis-à-vis the then Inventory worth to find out if the Possibility expires in-the-money or out-of-the-money.

Choices-Primarily based Funds: All this exercise should imply Choices Funds are Lively Funds

Choices-based funds must make 4 selections (perhaps 5 selections)

- What’s the fairness sleeve going to be?

- Is that this fund going to supply leverage, supply safety, or earn revenue?

- What’s the maturity of the choices expiry the supervisor chooses?

- What’s the strike worth of the choices the supervisor chooses?

The 5th selection: Ought to the choices traded match the Fairness sleeve?

However why do we’d like Choices Primarily based Funds? (a) Monetary Democratization

Regardless of the exponential improve in choices volumes over the a long time, many traders haven’t participated in choices. The jargon, the pricing, the buying and selling and execution, and a bunch of different obstacles have stored traders away.

The purpose of the administration groups providing Choices-based funds is to proceed on the journey of choices democracy. If skilled fund managers can supply their choices abilities, finish traders would possibly get the profit from the ability of choices with out paying the price of schooling. As a substitute, the associated fee is paid via a fund administration payment. This isn’t a lot completely different than Lively or Passive Funds charging traders a payment to place collectively an extended Fairness or lengthy Bond portfolio we name a “fund”.

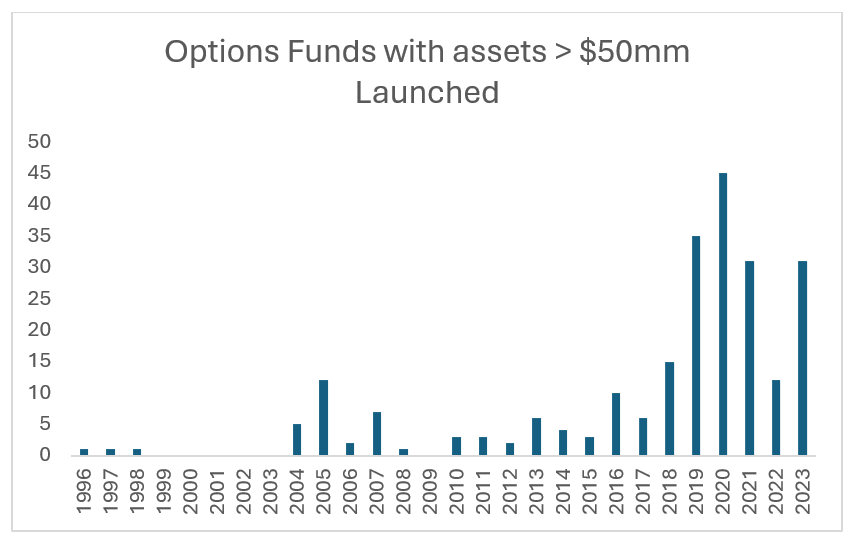

Because the chart under reveals us, Choices-based funds have picked up momentum beginning in 2018. The Y-axis reveals the variety of Choices funds with present belongings higher than $50mm began in every year.

However why do we’d like Choices Primarily based Funds? (b) A unique technique to obtain Portfolio Smoothing

Most of the readers shall be conversant in a 60/40 Inventory-Bond portfolio. When Shares zag, the hope is that Bonds will zig. Collectively, the portfolio shall be smoother. By diversifying throughout asset lessons (shares and bonds), and inside asset lessons (portfolio of shares), an investor hopes to earn the danger premium embedded in asset lessons whereas smoothening the journey.

Choices Primarily based Funds supply one more strategy to Portfolio Smoothing: 10 funds close-up

I requested @yogibearbull to outline Beta of an ETF/(inventory portfolio) to our readers.

He wrote, “beta of an ETF comes from linear regression of month-to-month returns with month-to-month benchmark returns (SP500 for US fairness funds). Beta is the slope, or short-term volatility; alpha is the intercept, or supervisor’s magic. An ETF with beta of 0.80 implies that if SP500 went up +1% that day, the ETF will seemingly go up +0.80%.”

Broadly talking, the decrease the beta of a portfolio, the decrease the volatility. Whereas a 60/40 lowers the portfolio’s total beta via the unfavourable correlation between shares and bonds, Choices funds decrease the beta via the collection of the Lively Sleeve and the Choices technique.

For instance, JHEQX, the JP Morgan Hedged Fairness Fund, an $18 Billion fund, has been round for 10 years. Listed below are the annual betas of this fund in accordance with Portfolio Visualizer:

| 12 months | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 ytd |

| Beta | 0.56 | 0.48 | 0.61 | 0.24 | 0.39 | 0.53 | 0.30 | 0.45 | 0.41 | 0.55 | 0.43 |

The Beta of JHEQX to the S&P 500 has by no means been larger than 61%. In actual fact, the typical Beta of the fund since 2014 has been 43%.

Thus, this fund would by no means make 100% of the returns of the S&P on the best way up AND would by no means lose as a lot because the S&P on the best way down.

For a lot of traders, this decrease beta is IMPORTANT. Why?

To be candid, traders wish to each be in US equities and never totally dedicated. Buyers are keen to commerce off some return for a smoother path.

Choices Primarily based Funds thus supply the promise of smoother returns.

The Many Shapes and Sizes of Choices Funds:

| On S&P 500 | On NDX | On Singles | On International | |

| Overwriting/Revenue | JEPIX/JEPI, GATEX, GSPKX, DIVO | JEPQ, QYLD | TSLY, NVDY, YieldMax ETFs | EXG, ETW, BOE |

| Hedged Fairness | JHEQX, JHQDX, BUFR | CIHEX | ||

| Put underwriting | GLSOX, IRONX |

This desk is one other technique to present the completely different methods employed by Fund managers and the completely different fairness sleeves. There are over 300 funds, so, that is only a gross classification. Every fund is constructed in a different way.

By Measurement

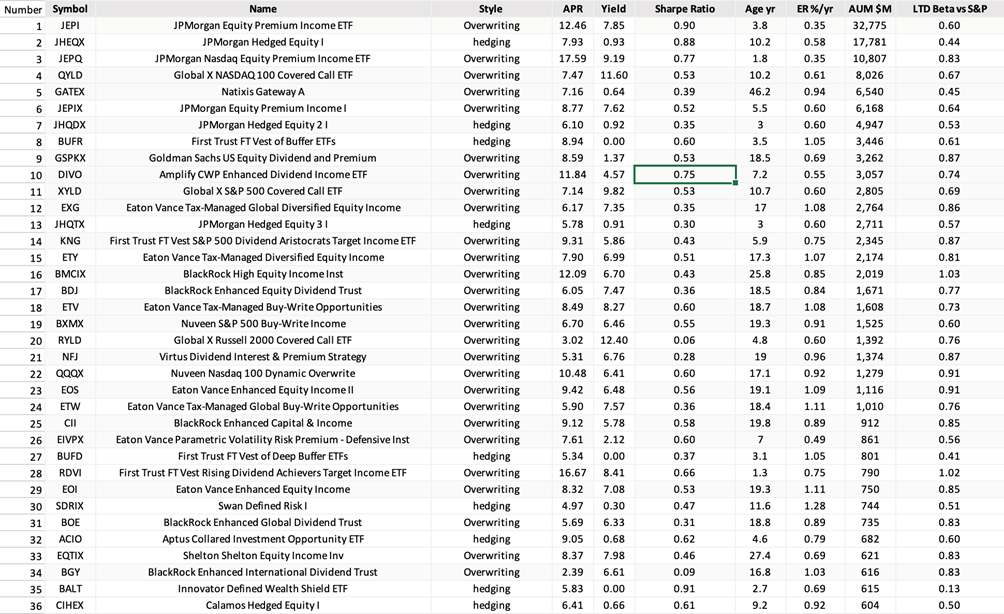

These are 23 funds with over $1bn USD AUM. I’ve created a desk with the highest 36 funds with belongings of $600 million and better.

Take a detailed have a look at the 4th column labeled APR (Annualized % Return).

Some funds like RYLD (Fund #20) have returned solely 3.02% a yr.

Others like JEPQ (Fund #3) have returned 17.59% per yr.

We additionally see that Yields (5th column) and Sharpe ratios (6th column) differ dramatically throughout funds.

Choices funds are fairly completely different sufficient of their make-up, which explains the variations in Returns, Yield, and Sharpe Ratios.

One factor we will depend on to be comparable for all these funds is an Expense Ratio that’s extra consistent with Actively Managed funds. 83bps common of all of the funds within the group excluding the biggest ETF, JEPI (Fund #1), which has an inexpensive expense ratio of solely 0.35%.

Let’s take a more in-depth have a look at a few of these funds. I’ve tried my finest to seize the essence of the funds. I’m taking slightly liberty with the small print to maintain us shifting:

- JEPI and JEPIX: JP Morgan Fairness Premium Revenue (#1 and #6 above)

The Open-ended fund, JEPIX was launched in Sep 2018, and the ETF, JEPI, in Might 2020. Collectively they maintain nearly $39B in belongings. Whereas the inventory portfolios are barely completely different between the fund and the ETF, they’re the identical to us. JEPI has a decrease Exp. Ratio than JEPIX.

The funds maintain a low beta, low volatility inventory portfolio. They intend to choose shares actively and maintain about 130 shares (not the five hundred shares within the S&P 500). Every week, the fund sells an ~2% Out-of-the-money name on the S&P 500 on ~ 20% of the Notional portfolio.

Such a fund employs a method often called “Coated Name Overwriting”. By promoting calls on 80% of the portfolio at any given time, they hope to earn revenue from the choice premiums. Together with the dividend earned on the underlying shares, these funds have a excessive distribution fee of between 8 to 12% since inception.

Why does this fund appeal to cash: Buyers like regular distributions from dividends and name premiums. They like the concept of selecting shares which have a decrease beta than the SPX. Buyers perceive their upside is capped in trade.

- DIVO: Amplify CWP Enhanced Dividend Revenue ETF (#10 above)

DIVO with $3B in Belongings additionally makes use of a Coated Name Overwriting. It has even fewer shares within the portfolio (28 shares). DIVO writes 1month name choices on a few of these shares (about 7 or 8 inventory choices).

We begin seeing how these merchandise differ. One writes calls on the S&P 500 Index, and the opposite writes name choices on some particular person shares.

One holds a low beta portfolio of 130 shares, the opposite holds solely 28 shares.

- GSPKX: Goldman Sachs US Eq Dividend and Premium (GSPKX) (Fund #9)

Been round since 2005 with belongings of about $3.5B. This fund is a Coated Name Overwriting just like JEPI/JEPIX. It holds 280 actively picked shares and sells Name Choices on the S&P 500 Index. The fund tries to protect the upside by overwriting ~40% of the Notional portfolio. When future volatility is excessive, and name costs are thus larger than common, the fund could promote as little as solely 15% of the Notional in name choices.

- BDJ: Blackrock Enhanced Dividend Belief (Fund # 17)

That is one among varied Blackrock funds that provides name overwriting together with lengthy equities. 80% of the $1.7 Bn fund is invested in US Equities and the remaining 20% within the UK and Europe. This fund’s fairness sleeve holds extra than simply US shares, which makes it completely different than the funds above. The fund overwrites part of the portfolio by promoting 1-2 month calls on a fraction of the shares. Like many different overwriting funds, Blackrock’s Funding strategy for this fund is constructed on 3 pillars: Portfolio constructed on Dividend development, Give attention to Excessive-High quality Firms, and Seeks to Scale back Portfolio Volatility.

- JEPQ: JPMorgan Nasdaq Fairness Premium Inc ETF (Fund #3)

Because the identify says, the fund is the Nasdaq 100 equal of JEPI and JEPIX (Fund #1 and Fund #6). The underlying shares are Nasdaq 100 shares (it truly holds 87 shares and Nasdaq futures) and it writes name choices on the Nasdaq 100 Index. The fund has $11.4B in belongings.

- QYLD: International X NASDAQ 100 Coated Name ETF (Fund #4)

Much like JEPQ in that the fund holds Nasdaq 100 shares. It sells a 1-month Nasdaq At The Cash Spot calls (that’s, every month it sells a name on the Nasdaq near the extent of the market on the time of buying and selling the decision choice). QYLD has $8.1B in belongings.

Every of those funds is a portray. The fund supervisor decides which underlying shares to purchase, hopes they’ve some alpha in inventory selecting (or they may personal the passive index), collects dividends, decides whether or not to promote name choices on the S&P 500, on the Nasdaq 100, or on a small part of the shares, what % of the notional portfolio to overwrite, and the size of those choices. Given the Belongings held by these funds, it’s secure to imagine that folks wish to put money into these name overwriting, income-generating, funds.

I’ve solely identified a number of of the bigger buy-write funds centered on US inventory portfolios. There are comparable funds on Rising Markets, on Worldwide Indices, and on International Indices. Nearly each financial institution affords their shoppers direct publicity to buy-write methods via Over-the-counter structured merchandise. The sizes contain dwarf the sizes in these listed funds. Earlier than we shut out the purchase writes, I’d wish to level out a fund technique that’s beginning to accumulate belongings shortly.

- YieldMax ETFs: TSLY, NVDY, APLY, CONY, OARK… (not within the desk above)

These funds personal only one inventory or ETF every – Tesla, NVIDIA, Apple, Coinbase, ARKK, and so forth. Every week they write out of the cash name choices expiring on the approaching Friday.

Their concept is to take the decision overwriting and the distribution from choice revenue to the acute. For example, NVDY, YieldMax™ NVDA Possibility Revenue Technique ETF, a $ 300mm fund holds $300mm of NVIDIA inventory and sells $300mm of weekly calls. Over a yr, if volatility stays excessive, the fund will overwrite NVIDIA 52 occasions (52 weeks). The distribution fee shall be 109.59% (that’s should you take what the fund pays out in revenue from choices offered and multiply by 12).

TSLY, YieldMax™ TSLA Possibility Revenue Technique ETF, has an annualized distribution fee of 62.7%.

What’s happening right here? There’s numerous choices hypothesis. Billions are being spent on Choices by all stripes of traders. This fund desires to promote to these consumers. There’s now over $2B within the over 15-20 ETFs provided by this fund household.

A latest article pointed to 2 accredited ETFs that may overwrite Zero-day choices every day. Should you like weekly overwriting, you’re going to love every day!

Shifting on, we subsequent have a look at some Hedged Fairness Funds now.

How is a Hedged Fairness fund just like and completely different than the Name Overwriting funds?

The similarity is within the Fairness sleeve, or the underlying shares, indices, or baskets held by Hedged Fairness Choices fund. Simply because the Overwriting funds may personal both the S&P 500, or the Nasdaq, or a small group of shares, or a world index, the identical goes for Hedged Fairness funds. They could possibly be passive or actively picked shares.

The distinction is how the 2 classes use Choices. Overwriting funds solely promote calls. Hedged Funds use Choices to supply a draw back buffer. Many funds are shopping for Places or Put Spreads to manage the losses of the Fairness Portfolio. Most of those funds will promote Calls to finance some or the entire prices related to shopping for the Places or Put Spreads.

By including Places/Put Spreads, the fund supervisor hopes to dampen the consequences of selloffs on an fairness portfolio. For some traders, clean returns are extra vital than massive returns. Though it’s the job of equities to generate volatility on the best way to incomes compounded returns, not everybody can take the volatility punches.

- GATEX: The Natixis Gateway Fund has been round since 2001 (Fund #5)

This $ 6.5B AUM fund owns 219 actively picked Shares + a put collar. A put collar is a mix of lengthy put and quick name.

The fund sells ~ 2-month S&P 500 name choices, that are ~2% out of the cash (that’s, 2% above the market degree on the time of promoting the choices), and it does so on 95% of the notional worth of equities held.

The fund additionally holds Put Choices on about 95% of the portfolio. The fund has purchased places on the S&P 500 Index, that are ~ 2 ½ months out and ~ 6.5% under the market degree.

- JHEQX/JHQTX/JHQDX: JPMorgan Hedged Fairness, Hedged 2, & Hedged 3 Fund (Fund #2, #7, and #13)

These are three completely different JP Morgan funds, similar to one another, and separated solely by a small twist. Collectively, they’ve $25 Billion in Belongings, making them one of many largest methods available in the market. All 3 funds maintain round 170 US large-cap shares (thus, actively managed).

If we dive deeper into one of many funds, JHEQX, which has been round since 2014, we see the fund owns a “Put-Unfold-Collar” (PSC). The fund owns a 3-month hedge by shopping for a 95% Put, promoting the 80% Put, and financing this Put-Unfold with a Name so the out-of-pocket is zero on the time of the commerce. This Strike of the decision relies upon upon the associated fee required to buy the 95-80 Put Unfold.

The thought is that an investor on this fund:

- Holds Actively Managed Giant Cap Equities (roughly just like the S&P 500)

- Earns the dividend

- Takes the inventory market threat for the 1st 5% of the portfolio

- Is protected beginning 5% all the best way to twenty% sell-off available in the market

- Then, takes the entire draw back as soon as once more after 20%

- Caps Fairness upside at roughly 6% from the present degree

JHEQX executes this Put Unfold Collar each 3 months in Dec, March, June, and Sep.

The opposite funds, JHQTX and JHQDX, do it Jan, April, July, October and Feb, Might, Aug, Nov respectively. There aren’t any different conceptual variations between these funds.

Having $25 Billion in a method is not any joke. This tells us that the market yearns for a product like this. Thus, we now see tons of of funds that provide some type of “Hedged”, “Buffered”, “Capped”, “Protected” of their funding mandate.

- BUFR: First Belief FT Vest of Buffer ETFs (Fund #8)

A closing instance of a Hedged fund is BUFR. The ETF itself is made up of 12 month-to-month ETFs, so it’s a fund of funds. It owns an equal 8.33% weight in funds FJAN, FBEB, FMAR….FDEC.

FJAN is itself made up of solely 4 1-year choices. If we peel the union FJAN is:

- Lengthy the S&P 500 Index (it does this via choices)

- Lengthy a 100-90 Put Unfold (versus the 95-80 Put unfold we noticed above)

- Brief a Name 13-14% above the market

As a result of it holds no shares in any respect and replicates its lengthy S&P 500 Index publicity via Choices, there are some funky issues this FJAN and thus BUFR can do which enhance tax remedies for a really particular group of traders.

FJAN alone has $750 million in Belongings and BUFR has $3.5 Billion in belongings.

The identical fund supervisor affords Buffer, Average Buffer, and Deep Buffers for each single month and tens of different ETFs.

Variety of the Many

Every of those funds is a portray. The fund supervisor decides which underlying shares to purchase, hopes they’ve some alpha in inventory selecting (or they may personal the passive index), collects dividends, decides whether or not to promote name choices on the S&P 500, on the Nasdaq 100, or on a small part of the shares, what % of the notional portfolio to overwrite, and the size of those choices. Within the Hedged funds, the supervisor will wish to personal places or put spreads together with the entire above.

Conclusion

The purpose so far within the article was to pick some massive funds and present how they’re comparable and completely different to one another. I hope the reader has a way of the variety in these funds.

Variety and selection are a good suggestion, however does it generate income? Is it financially good? How can we examine such completely different funds to determine if they’re a wise funding?

We hope to take a look at that within the 3rd article.

{kind=link}