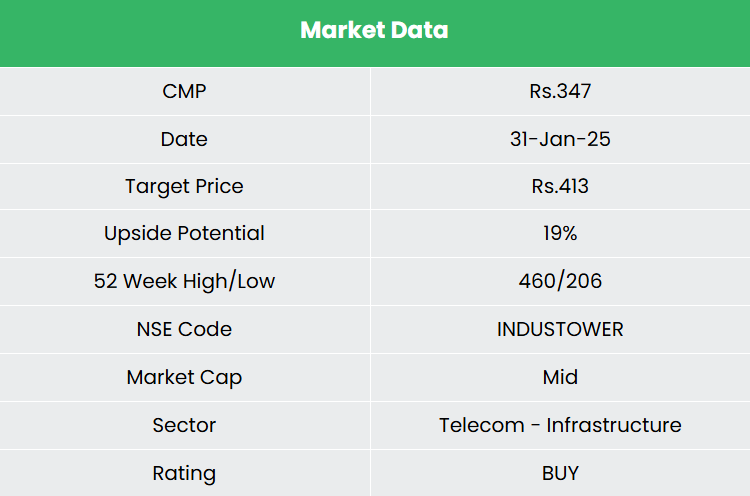

| Alpha StockInsights")

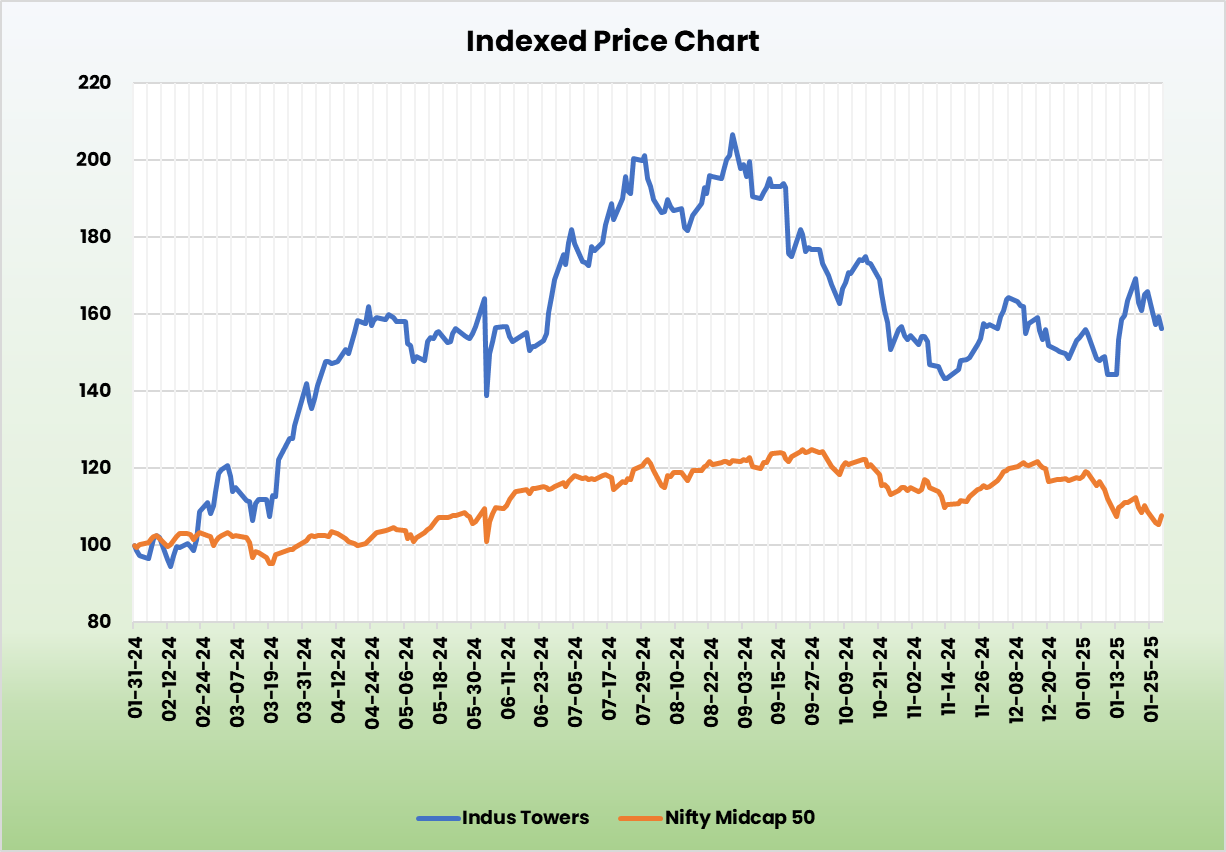

Indus Towers Ltd – Connecting Lives Throughout the Nation

Indus Towers Ltd., shaped by means of the merger of Indus Towers and Bharti Infratel, is without doubt one of the largest telecom tower firms globally. Established in 2006 and headquartered in Gurugram, the corporate supplies tower and associated infrastructure-sharing companies, managing the deployment, possession, and operation of passive infrastructure for telecom networks. As of December 31, 2024, Indus Towers operates over 234,643 macro towers and 386,819 macro co-locations, with a presence throughout all 22 telecom circles in India. Its shopper base contains {industry} giants akin to Bharti Airtel (together with Bharti Hexacom), Vodafone Thought Restricted (VIL), and Reliance Jio Infocomm Restricted.

Merchandise and Companies

The corporate’s services and products are centered round 3 core parts:

- Tower – For mounting the operator antennae at an applicable top, encompassing a variety of designs from ground-based towers and rooftop towers to hybrid poles and monopoles.

- Energy – For offering uninterrupted power provide to telecom gear together with greener power options.

- Area – Collaboration with residential and business property house owners for housing telecom and energy gear.

Subsidiaries: As of FY24, the corporate has 1 subsidiary and no associates/joint ventures.

Funding Rationale

- Market chief – Indus Towers is the main supplier of tower infrastructure within the nation, serving high Telecom Companies Suppliers (TSPs). It primarily gives shared entry to its towers for wi-fi telecommunications suppliers by means of long-term contracts. The corporate is steadily growing its market share, fuelled by the speedy rollout of 5G companies by TSPs, which has considerably boosted its income. Moreover, the continued growth into rural areas by main purchasers is predicted to create additional progress alternatives. The corporate at the moment serves all telecom suppliers throughout India and has a presence in all 22 telecom circles nationwide. With an industry-leading tenancy ratio of 1.65x, Indus stays a dominant drive within the sector. The corporate can be constantly reaching steady monetary efficiency underpinned by strong tower and co-location additions. Throughout Q3FY25, it added 4,985 macro towers and seven,583 macro co-locations.

- Development methods – The corporate has collected vital overdue from VIL. It has additionally secured a big share of the roll out by VIL. The corporate can be specializing in optimising its energy and gas price (which is a serious contributor of the corporate’s working expense) by means of decreasing diesel price and growing the usage of photo voltaic power. The corporate’s photo voltaic websites at the moment stand at 28,000 which was 25,000 through the earlier quarter. It has additionally entered into an influence buy settlement with a strategic accomplice for procurement of renewable power of 130 MW photo voltaic plant by way of a 26% acquisition of stake at a consideration of Rs.38 crore. It is usually transitioning its battery portfolio to lithium-ion batteries which has decrease charging time and an extended life. The corporate is pivoting in the direction of an elevated share of lighter tower variant. These strategic initiatives are anticipated to enhance working and value efficiencies. The corporate plans to foray into the EV charging infrastructure sector and has launched its pilot companies within the enterprise hub of Gurugram and the southern metropolis of Bengaluru.

- Q3FY25 – Through the quarter, the corporate generated income of Rs.7,547 crore, a rise of 5% in comparison with the Rs.7,199 crore of Q3FY24. Working revenue elevated from Rs.3,622 crore of Q3FY24 to Rs.6,997 crore of Q3FY25, a progress of 93%. The corporate reported web revenue of Rs.4,003 crore, a rise by 160% YoY. The earnings have been influenced by the gathering of overdues and assortment of Rs.19.1 billion from monetization of the secondary pledge on shares by VIL within the firm. Adjusting to this, EBITDA and web revenue has improved by 8% every through the quarter.

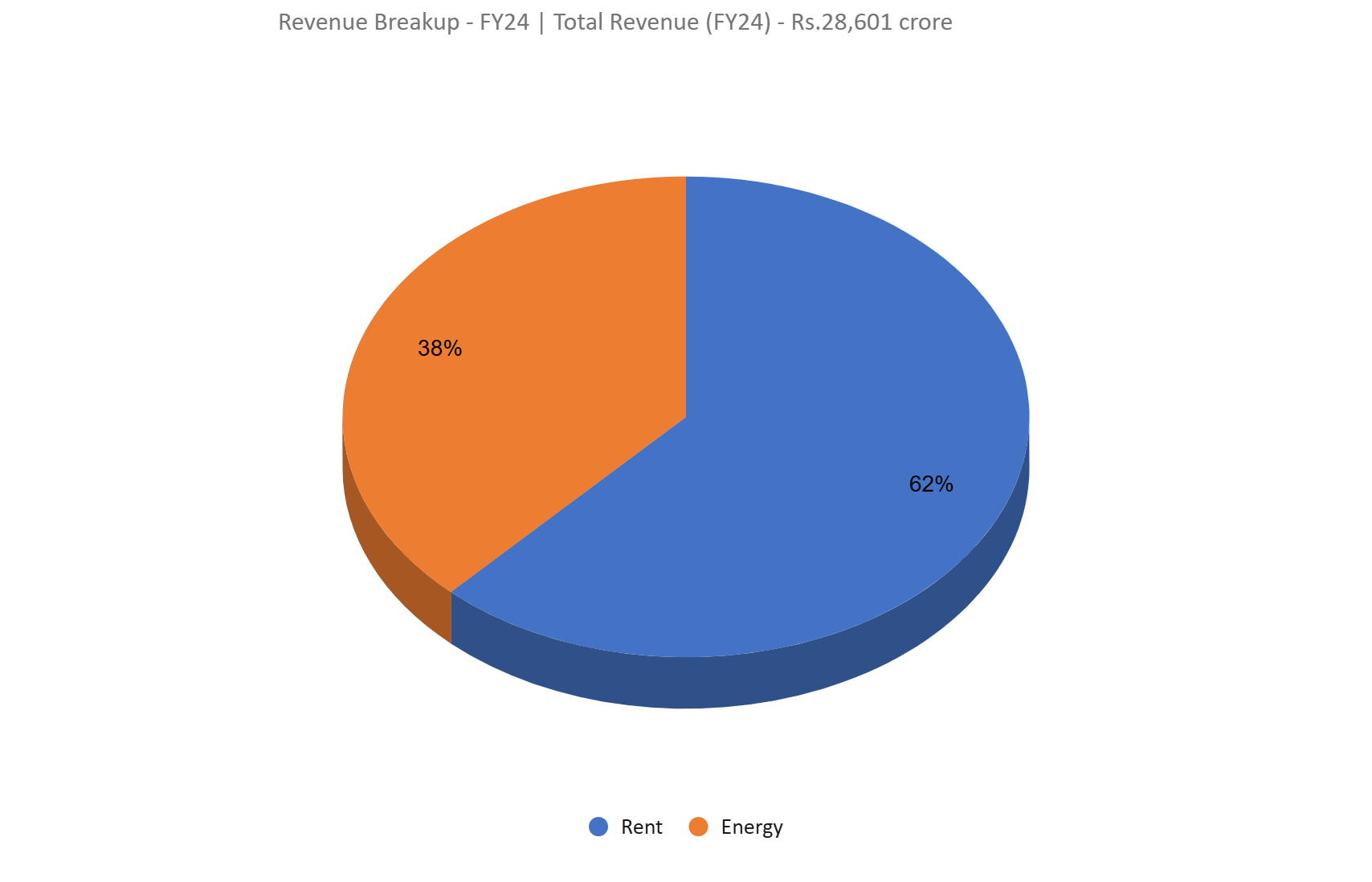

- FY24 – Through the FY, the corporate’s income was flat at Rs.28,601 crore. Working revenue was at Rs.14,694 crore, up by 50% YoY. The corporate reported web revenue of Rs.6,036 crore, a rise of 196% YoY. Through the monetary 12 months, the corporate crossed 2 lakh towers in its portfolio.

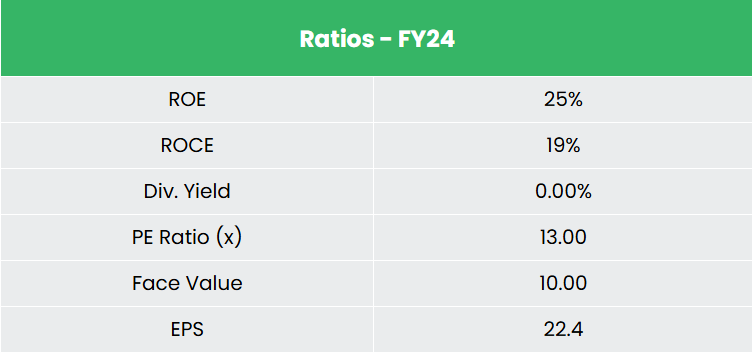

- Monetary efficiency – The corporate has generated income and web revenue CAGR of 27% and 17% over the interval of three years (FY21-24). Common 3-year ROE & ROCE is round 22% and 19% for FY21-24 interval. The corporate has a sturdy capital construction with a debt-to-equity ratio of 0.75.

Trade

The telecommunications {industry} in India is without doubt one of the fastest-growing sectors and a serious contributor to employment, rating among the many high 5 job turbines within the nation. Inexpensive tariffs, roll-out of Cellular Quantity Portability (MNP), evolving consumption patterns of subscribers, authorities’s initiatives in the direction of digitization are bolstering India’s home telecom manufacturing capability, and a conducive regulatory surroundings lays sturdy basis for exponential progress within the {industry}. As of Might 2024, India is the second-largest telecommunications market globally, with a complete of 1,203.69 million phone subscribers. Nevertheless, rural tele-density stands at simply 59.59%, presenting a big progress alternative on this underserved space. Moreover, India is already laying the groundwork for 6G by investing within the know-how’s growth.

Development Drivers

- In Union Price range 2024-25, the Division of Telecommunications and IT was allotted Rs.116,342 crore (US$ 13.98 billion).

- Authorities initiatives akin to 100% FDI allowed underneath the automated route, PLI for Telecom and Networking gear, Digital Bharat Nidhi Fund, lowered license charges, and spectrum liberalization.

- Rising inhabitants and a quickly growing web penetration price with is predicted to drive the demand for telecom companies.

Peer Evaluation

Rivals: Suyog Telematics Ltd, Sar Televenture Ltd and so on.

In comparison with the above opponents, Indus Towers stands out as essentially the most undervalued inventory on this phase. The corporate is constantly translating its regular progress in gross sales into increasing margins and earnings.

Outlook

The corporate’s 4 strategic priorities are: a) growing market share, b) enhancing price effectivity by optimizing diesel utilization, c) making certain community uptime, and d) selling sustainability. Through the previous 12 months, the widespread rollout of 5G companies by operators has pushed greater income streams and fuelled sturdy progress for the corporate. Components that might drive progress embody large-scale nationwide operations in an {industry} with vital entry limitations, the growing potential for information consumption and the rise in information customers/gadgets, a powerful presence throughout all telecommunications circles, and long-term contracts with purchasers.

Valuation

The demand for telecom infrastructure is predicted to remain sturdy, pushed by excessive information consumption, speedy 5G rollouts, and the present community hole in 4G companies. We consider Indus Towers Ltd. is well-positioned to reap the benefits of these traits. We advocate a BUY score within the inventory with the goal value (TP) of Rs. 413, 16x FY26E EPS.

Threat

- Monetary stability of TSPs – The rising investments in 5G rollout, together with different companies and spectrum acquisitions, are placing stress on TSPs’ financials. This might doubtlessly have an effect on their capability to make funds to Indus Towers, which could, in flip, impression the corporate’s monetary efficiency.

- Unfavourable phrases for contract renewal – Any unfavourable adjustments to the contract phrases with the shopper, akin to decrease pricing or annual value escalations when renewing leasing agreements, pose a threat to the corporate.

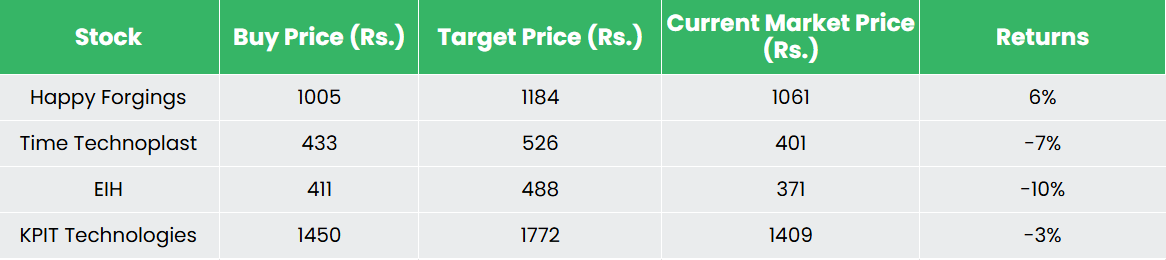

Recap of our earlier suggestions (As on 31 January 2025)

Completely satisfied Forgings Ltd

Disclaimer: Investments within the securities market are topic to market dangers, learn all associated paperwork rigorously earlier than investing. Securities quoted listed here are exemplary, not recommendatory. Please seek the advice of your monetary advisor earlier than investing. Please notice that we don’t assure any assured returns for the securities quoted right here.

Analysis disclaimer: Funding within the securities market is topic to market dangers. Learn all of the associated paperwork rigorously earlier than investing. Registration granted by SEBI, and certification from NISM under no circumstances assure the efficiency of the middleman or present any assurance of returns to traders.

For extra particulars, please learn the disclaimer.

Different articles you could like

Submit Views:

2,307

{kind=link}