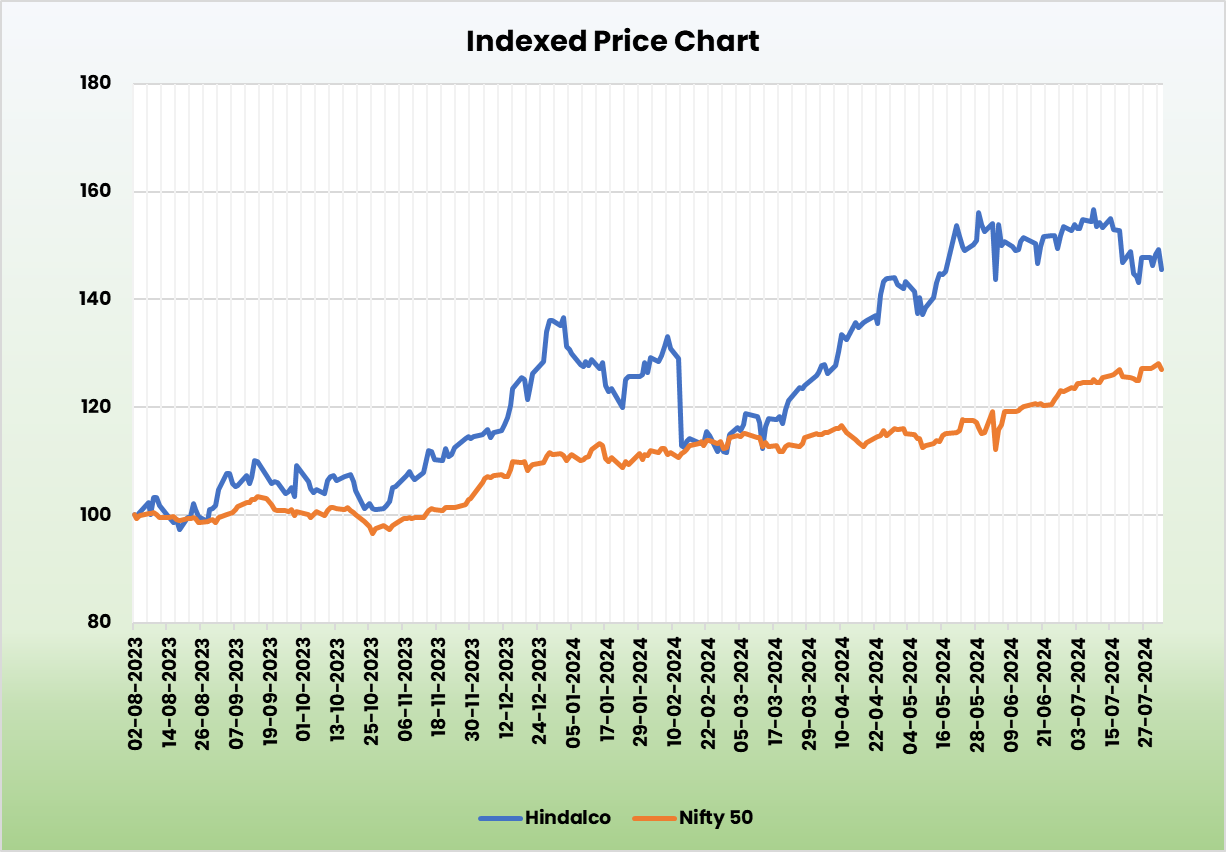

Hindalco Industries Ltd – A power for good

Hindalco Industries Ltd, a part of the Aditya Birla Group, is a world chief in aluminium rolling and recycling, and a serious participant in copper and speciality alumina. Its built-in enterprise mannequin covers bauxite mining, alumina refining, coal mining, energy technology, aluminium smelting, and downstream merchandise. As of FY24, Hindalco operates 20 manufacturing items and 23 mines in India, together with 32 abroad vegetation (Novelis).

Merchandise and Providers

- Aluminium: Providing alumina, main aluminium (ingots, billets, wire rods), and flat rolled merchandise (foils, extrusions).

- Copper: Producing LME grade copper cathodes, steady solid copper rods, di-ammonium phosphate (DAP) fertiliser, and treasured metals (gold and silver).

- Specialty Alumina: Offering coarse alumina hydrate, metallurgical alumina, specialty alumina, and alumina hydrate.

Subsidiaries: As of FY24, the corporate has 61 subsidiaries, 7 affiliate firms, 2 joint ventures and 6 joint operations.

Progress Methods

- Novelis Enlargement: Investing $4.9 billion over 3-5 years, together with $4.1 billion for a brand new Bay Minette facility to extend Flat Rolled Merchandise capability by 600 KT.

- Capability Enhance: Accomplished a debottlenecking challenge at Utkal, elevating alumina capability from 2.2 million MTPA to 2.6 million MTPA.

- New Tasks: Growing an 850 KT refinery in Odisha and commissioning a 20 KT precipitate hydrate plant by FY25.

- Product Innovation: Enhancing merchandise with new choices comparable to white fused alumina, excessive precision sub-micron alumina, and battery-grade aluminium foil.

- International Enlargement: Establishing warehouses, processing services, and gross sales workplaces throughout the USA, Europe, and Southeast Asia.

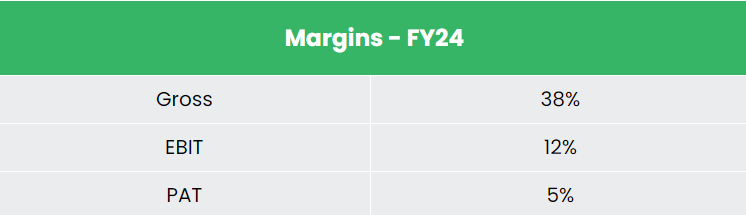

Monetary Efficiency

Q4FY24

- Income: Flat at Rs.55,994 crore YoY.

- EBITDA: Elevated by 24% to Rs.7,201 crore from Rs.5,818 crore in Q4FY23.

- Internet Revenue: Grew by 32% to Rs.3,174 crore from Rs.2,411 crore in Q4FY23.

- Efficiency Drivers: Strong restoration at Novelis, improved value management within the aluminium India enterprise, and powerful copper enterprise efficiency.

- Shipments Progress: Novelis +2% YoY, Aluminium Upstream +4% YoY, Aluminium Downstream +17% YoY, Copper +16% YoY.

FY24

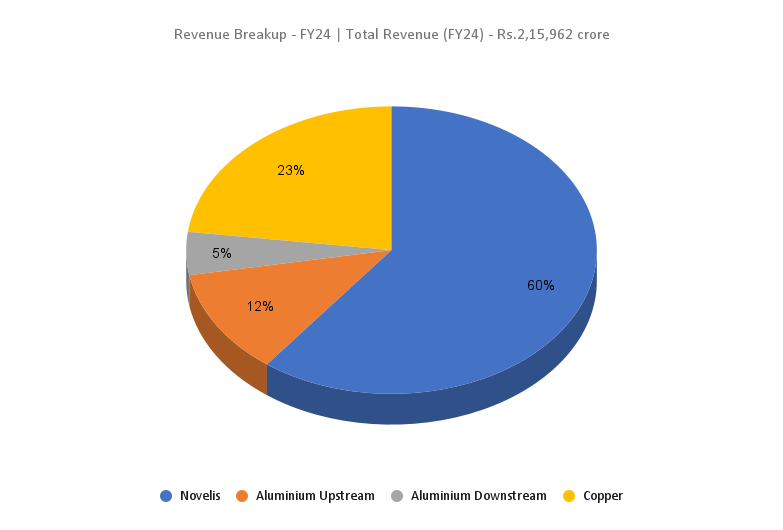

- Income: Rs.2,15,962 crore, down 3% YoY.

- Working Revenue: Rs.25,728 crore, up 7% YoY.

- Internet Revenue: Rs.10,155 crore, up 1% YoY.

- New Launches: 53 new services and products launched.

Monetary Efficiency (FY21-24)

- Income and PAT CAGR (FY21-24): 18% and 40%, respectively

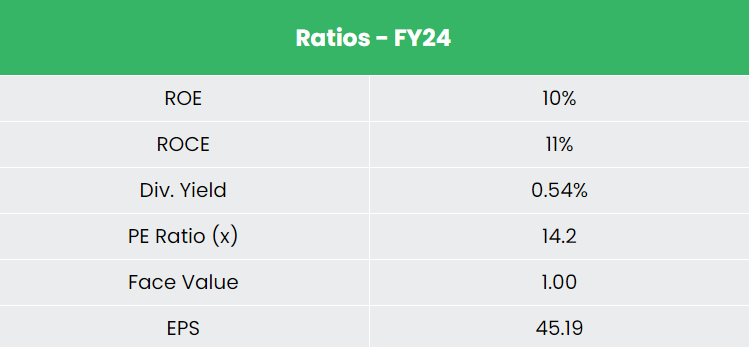

- Common 3-12 months ROE & ROCE (FY21-24): ~13% every

- Capital Construction: Debt-to-equity ratio of 0.53

Business outlook

- Financial Impression: The mining business can enhance GDP, overseas change earnings, and help sectors like constructing, infrastructure, automotive, and electrical energy by offering important uncooked supplies cost-effectively.

- Power Demand: Because the third-largest vitality client globally, India faces excessive demand for energy and electrical energy, resulting in elevated coal demand.

- Alumina Benefit: India advantages from low alumina manufacturing and conversion prices and ranks because the second-largest international producer of aluminium.

- International Aluminium Demand: Anticipated to develop by 3% in CY2024, reaching round 72 million MT.

- Copper Demand: International refined copper demand is projected to extend by roughly 2.5% in CY2024.

Progress Drivers

- FDI Coverage: 100% overseas direct funding (FDI) allowed by the automated route within the mining sector.

- Authorities Initiatives: Packages like Gati Shakti Grasp Plan, Make in India, Pradhan Mantri Awas Yojna, and City Infrastructure improvement schemes are anticipated to spice up the Metals and Mining sector’s progress in India.

Aggressive Benefit

Nationwide Aluminium Firm Ltd is the only real listed competitor with comparable operations.

In comparison with it, Hindalco exhibits extra steady return ratios and superior income and revenue progress, reflecting higher monetary stability and effectivity in producing returns.

Outlook

- Income: Flat progress; EBITDA improved throughout main segments.

- Efficiency Drivers: Larger volumes, higher margins, strategic product combine, steady operations, and powerful copper enterprise.

- Investments: ~$2 billion for India operations, specializing in downstream expansions (3-5 years).

- Alumina Manufacturing: Planning to double capability by FY26-27.

- Coal Provide: Acquired two captive coal mines to boost provide chain and coal high quality.

Valuation

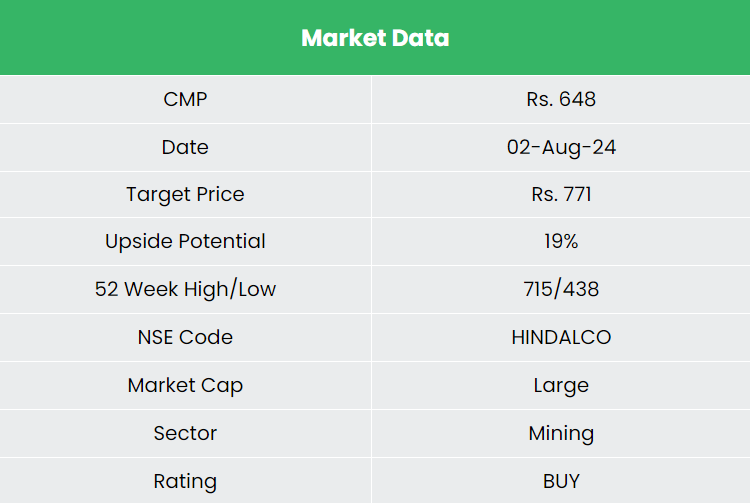

Hindalco’s dedication to growth, robust steadiness sheet, strategic capex plans, and confirmed execution—amid sturdy demand in packaging, automotive, transport, constructing, building, and industrial equipment—are anticipated to boost future efficiency. We advocate a BUY ranking with a goal worth of Rs.771, based mostly on 13x FY26E EPS.

Dangers

- Environmental and Social Impression: Mining actions could pose vital environmental and social challenges.

- Enter Prices: Fluctuations in home useful resource availability (notably coal) and uncooked materials costs might have an effect on revenue margins.

Word: Please observe that this isn’t a suggestion and is meant just for academic functions. So, kindly seek the advice of your monetary advisor earlier than investing.

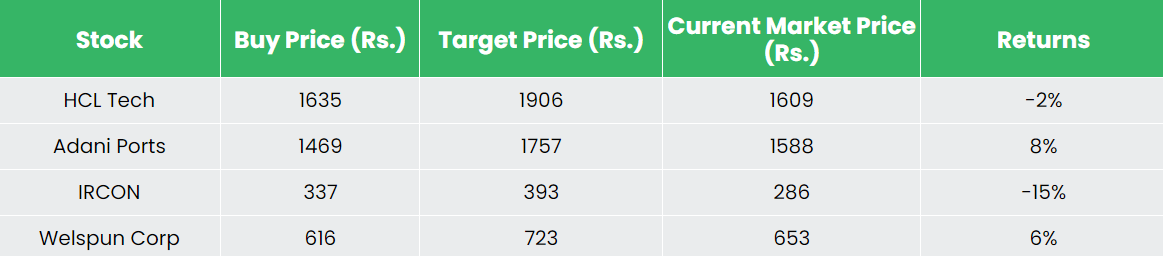

Recap of our earlier suggestions (As on 02 August 2024)

Adani Ports & Particular Financial Zone Ltd

Different articles chances are you’ll like

Publish Views:

541

{kind=link}